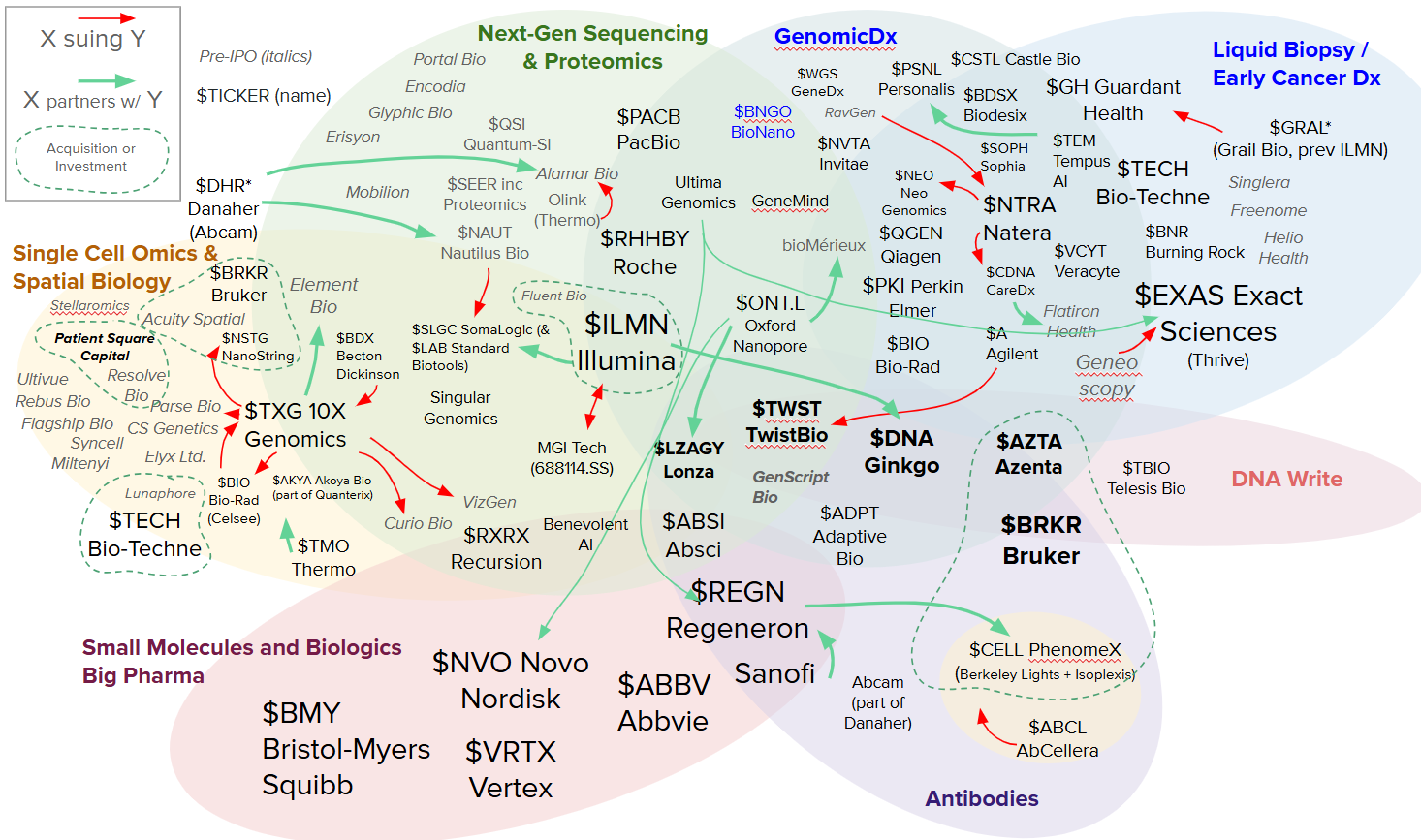

NGS and Multi-Omics M&A 1-2 year moves

Below I evaluate potential near-term (1–2 year) M&A moves by Thermo Fisher, Danaher, Revvity (PerkinElmer), QIAGEN, bioMérieux, Bruker, and Bio-Rad, focusing on acquisitions of NGS platform companies (Ultima, ONT, PacBio, Element, Singular) and multi-omics firms (e.g. 10x Genomics). Each scenario is weighed for strategic fit, technological synergy, financial feasibility, and market positioning of the acquirer. We also account for recent developments (e.g. Roche SBX) and the absence of Chinese players in Western deal-making. In the final section, I highlight the top 3–5 most probable M&A scenarios with an estimated likelihood.

Thermo Fisher Scientific (TMO)

Thermo Fisher has a broad life-science toolkit and strong financial firepower. In 2024 alone it generated $8.7B in operating cash flow and spent $3.1B on M&A (e.g. acquiring Olink Proteomics). Thermo already owns the Ion Torrent NGS line (short-read semiconductor sequencers), but Ion Torrent remains a niche clinical player with minimal R&D investment. To truly compete with Illumina’s stronghold, Thermo is likely eyeing next-gen platforms that offer either ultra-low sequencing costs or long-read capabilities:

Ultima Genomics (UG) – Ultra-high-throughput, low-cost short reads. Ultima’s technology promises whole genome sequencing for ~$80-100. Thermo’s involvement in the UK Biobank proteogenomics project – which chose Ultima’s UG100 as the sequencing engine – suggests a close relationship. Industry observers note Thermo’s “cash tsunami” could readily fund a deal, and having a <$100/genome platform would be transformative for Thermo if Ultima delivers on its promise. The strategic fit is clear in terms of disrupting Illumina’s cost leadership. However, Thermo is disciplined about profitability, and Ultima (still in early commercialization) isn’t profitable yet. Verdict: Thermo acquiring Ultima is plausible – a bold bet on NGS cost leadership. The presence of Thermo’s former COO Mark Stevenson on Ultima’s board (he “continues to serve on Thermo’s advisory board”) underscores the strong ties and has fueled speculation of a deal.

Element Biosciences (EB) – Benchtop short-read sequencers. Element’s AVITI system targets the mid-throughput segment with flexibility and lower operating costs. With ~$60M revenue in 2024, Element is further along commercially (and likely lower risk) than Ultima, but Element did raise a lot of money in subsequent rounds, including a recent one only months ago. Some analysts argue Element could be a “better target” for Thermo than Ultima if Thermo wants to plug a near-term gap in its sequencing portfolio. Acquiring Element would give Thermo a modern short-read platform to offer its clinical and research customers, complementing or eventually replacing the aging Ion Torrent line. Another factor to consider is the Multi-Omics play that Element Bio is laying out with the Teton kits, which would give Thermo’s sales team a more broad array of products to sell to potential clients. Verdict: Also quite possible – Thermo could view Element as an immediate boost in NGS offerings (with consumable revenues) versus the more speculative but higher-upside Ultima. Thermo might even pursue both a short-read platform (Element or Ultima) and a long-read platform over time.

Pacific Biosciences (PacBio) – Long-read, hi-fi sequencing. PacBio would give Thermo a leading long-read technology (SMRT sequencing) to pair with its short-read franchise. Thermo was previously rumored as a potential PacBio suitor after Illumina’s attempted takeover was blocked. Now PacBio’s situation may make it more approachable: after launching its Revio and more recently the Vega systems, PacBio’s sales have been flat and its stock has plummeted, losing ~65% of value in the past year. Industry chatter suggests PacBio could be “in a death spiral” and even “must be for sale” given its cash burn and 2-year runway. Thermo could certainly afford PacBio (market cap now only a few hundred million), instantly rounding out a full spectrum sequencing portfolio (short- and long-read). The main hesitation might be cultural and technological fit – SMRT sequencing is quite distinct from Thermo’s current platforms, and PacBio isn’t yet proven in terms of commercial success for clinical diagnostics. Verdict: Thermo acquiring PacBio is a moderate likelihood scenario if Thermo prioritizes long-read capability. Thermo would gain highly differentiated tech (ultra-accurate long reads) and could invest to finally drive PacBio into clinical markets. (Danaher, however, may be even more likely for PacBio – see below.)

Oxford Nanopore Technologies (ONT) – Real-time single-molecule (nanopore) sequencing. ONT’s portable sequencers (e.g. MinION, PromethION) offer long or ultra-long reads and rapid deployment (used in the field for Ebola, COVID-19, etc.). Thermo could leverage ONT’s tech to offer real-time sequencing solutions for clinical and applied markets. ONT’s current market value (~$1–1.5B) is within Thermo’s reach. The strategic fit is somewhat overlapping with PacBio (both cover long reads) – Thermo would likely choose one or the other. ONT’s nanopore platform might appeal for its speed and unique applications, though its accuracy still trails PacBio’s. Verdict: Possible but less emphasized than Ultima/Element. Thermo already sells sample prep and reagents widely used with ONT sequencers, so it may opt to partner rather than buy. If Thermo’s goal is to dominate clinical long-read sequencing, acquiring PacBio (for accuracy) or ONT (for speed) are two paths – of these, PacBio’s low price and existing SoftBank investment may make it a more straightforward acquisition target in the near term.

Thermo Summary: Expect Thermo Fisher to make at least one significant NGS acquisition in the near term, given its resources and stated growth plans. A short-read platform acquisition (Ultima Genomics or Element Biosciences) is highly likely to strengthen Thermo’s hand against Illumina’s core business (Thermo’s huge cash generation supports this move). A long-read play (PacBio or ONT) is also on the table, especially if valuations remain attractive – Thermo could thereby offer end-to-end sequencing solutions (much as Illumina is trying to do via its own platforms and collaborations). Thermo’s focus on clinically oriented, profitable businesses might tilt it slightly toward Element (which has growing sales) in the short term, but the strategic allure of Ultima’s $100 genome or PacBio’s HiFi reads is undeniable. Overall, Thermo Fisher is one of the most likely acquirers of an NGS upstart within 1–2 years.

Danaher Corporation

Danaher, a conglomerate spanning life science tools and diagnostics, has both ample capital and a track record of aggressive M&A. In recent years Danaher spent $9.6B for Aldevron (2021) and $5.7B for Abcam (2023), on top of prior deals (Cytiva from GE, IDT, Cepheid, Beckman Coulter, etc.). Danaher currently lacks an in-house NGS platform, but it serves genomic researchers through consumables (IDT’s oligonucleotides), automation (Beckman), and diagnostics (Cepheid’s PCR systems). With NGS increasingly used in clinical settings (e.g. oncology, infectious disease), Danaher is a prime candidate to acquire an NGS or single-cell sequencing company to round out its portfolio. Key targets and fit:

10x Genomics (TXG) – Single-cell and spatial genomics leader. 10x doesn’t make sequencers, but its Chromium platforms produce libraries for NGS (single-cell RNA-seq, ATAC-seq, etc.), and its emerging Visium/Xenium spatial biology tools are multi-omic by nature. For Danaher, 10x would bring a high-growth consumables business (hundreds of millions in annual revenue) and a dominant franchise in single-cell analysis – highly complementary to Danaher’s lab instrument businesses. Importantly, 10x’s products create demand for sequencing; owning 10x could be Danaher’s beachhead into the NGS workflow even without owning a sequencer (though Danaher could later pair 10x with an NGS platform acquisition). Financially, 10x’s stock has been beaten down – its market cap is only ~$1.3B as of early 2025 (down from >$10B at its peak), making it a ripe target. Danaher can easily absorb a deal of this size. The strategic fit is excellent: Danaher’s Beckman unit even partners with 10x (automation of 10x assays on Beckman liquid handlers). The main question is likelihood – many analysts view 10x as one of the most likely M&A targets in life sciences given its platform status and current valuation. Danaher is frequently mentioned as a logical acquirer, as it could plug 10x into its Life Sciences segment and scale it globally. Verdict: Very high probability. Danaher acquiring 10x Genomics would unite complementary strengths (instruments + single-cell reagents) and align with Danaher’s strategy of owning unique, consumable-rich tool franchises. This scenario is widely speculated and could easily materialize if 10x remains undervalued.

Pacific Biosciences (PacBio) – PacBio is also on Danaher’s radar. When Illumina’s $1.2B bid for PacBio fell through in 2020, Cowen analysts specifically listed Danaher (and Agilent/Thermo) as potential PacBio buyers. PacBio would give Danaher a cutting-edge sequencing instrument line (Revio and Vega long-read sequencers and the Onso short-read platform in development) to slot into its Diagnostics or Life Sciences segment. Danaher has the expertise to drive PacBio’s technology into clinical labs (leveraging its diagnostics sales channels). Given PacBio’s current struggles – flat sales and ongoing losses leading to drastic cost cuts – an acquisition could be mutually beneficial. PacBio’s valuation (~$0.4B) is a bargain relative to its rich IP and technology, though Danaher would need to invest significantly in marketing and support to realize PacBio’s potential. Culturally, integrating an R&D-heavy platform company fits Danaher’s playbook (they have successfully integrated tech-focused firms before). Verdict: High probability. PacBio fits Danaher’s model of acquiring differentiated technology leaders. With PacBio’s shareholders (including SoftBank) likely frustrated by poor stock performance, Danaher could swoop in. This move would instantly position Danaher as a direct Illumina competitor in sequencers – a bold but plausible strategic shift given Danaher’s ambition in genomics. PacBio might be Danaher’s Plan B if a 10x Genomics deal doesn’t happen first (or conceivably, Danaher could attempt both over a couple of years, given its capacity).

Oxford Nanopore (ONT) – ONT’s long-read, portable sequencing platforms could also tempt Danaher. Acquiring ONT would give Danaher unique real-time sequencing tech and a strong presence in applied markets (e.g. infectious disease surveillance, where ONT has seen adoption). ONT’s London listing might complicate a takeover (UK regulators could scrutinize foreign acquisition of a “national champion”), but it’s feasible, especially considering that the “golden share” option has recently expired. Still, Danaher may prioritize PacBio for accuracy or 10x for market share. Given the current specs for ONT’s technology, it would require significant support and continuous improvement post acquisition (something ONT has managed well so far on their own); Danaher’s decentralized model could either help by providing resources or potentially hinder ONT’s innovative culture. Verdict: Moderate probability. ONT is a strategic asset that any big player must consider, but Danaher might find 10x or PacBio a more straightforward fit. If PacBio were off the table, Danaher could eye ONT as the next best way to own long-read sequencing.

Ultima Genomics / Element Biosciences – Danaher tends to acquire companies with established revenues or clearly defensible tech. Ultima (still pre-commercial for the most part) might be too speculative for Danaher’s taste, and Element, while commercial, is relatively small. Danaher could consider Element if it wanted a benchtop NGS system to offer alongside its lab automation and genomics consumables, but this seems less likely than the marquee targets above. Ultima’s cost-disruptive angle is intriguing, yet Danaher usually avoids unproven bets. Verdict: Low probability for now. Danaher’s M&A dollars will likely target bigger fish (10x, PacBio) that provide immediate market share or unique content.

Danaher Summary: Danaher is arguably the most likely acquirer of a genomics tools company in this space, given its M&A hunger and the clear strategic fits available. 10x Genomics stands out as a top target – it aligns perfectly with Danaher’s focus on high-growth, consumable-heavy businesses, and would expand Danaher’s reach into the single-cell and spatial genomics boom. An acquisition of PacBio is also highly plausible, allowing Danaher to leap directly into the NGS instrument arena with leading long-read technology (especially now that PacBio is affordable and needs a stable parent to thrive). Danaher could thereby offer an end-to-end genomics workflow (sample prep via Cytiva/IDT, sequencing via PacBio, single-cell via 10x, analysis software via its diagnostics arm), which is strategically compelling. We assign a very high likelihood to Danaher making a major move (one of the above) in the next 1–2 years.

QIAGEN

QIAGEN is a leader in sample preparation and clinical diagnostic assays (especially in oncology and infectious disease), but notably does not have a successful in-house NGS platform today. It did launch the GeneReader NGS system in 2015 as a “sample-to-insight” clinical sequencing solution, but that effort struggled against Illumina’s IP dominance. By 2019 QIAGEN halted further sequencer development and took a $200M charge to exit its GeneReader initiative. Since then, QIAGEN has focused on NGS library prep kits and bioinformatics, partnering with sequencing platform companies rather than building its own. However, the growing demand for clinical NGS (e.g. comprehensive tumor profiling, liquid biopsy tests) means QIAGEN may want to own a sequencing platform to pair with its extensive menu of assays and reagents. With Chinese players constrained, QIAGEN could seize a Western technology to bolster its long-term competitiveness. Potential acquisition angles:

Element Biosciences – Element’s mid-throughput AVITI sequencer could suit QIAGEN’s customer base of regional hospitals and labs. QIAGEN could integrate Element’s instrument with QIAGEN’s sample prep, panels, and reporting software to deliver a turnkey clinical NGS solution (much like it intended with GeneReader). The strategic fit is straightforward: QIAGEN excels at kits and clinical market access, while Element provides the hardware. Financially, Element (a private company with ~$25–60M revenue) might be obtainable at a few hundred million dollars – within reach for QIAGEN (market cap ~$10B) and far less than QIAGEN’s own failed internal investment. Verdict: Moderate probability. If QIAGEN’s management is willing to re-enter the sequencing platform arena, acquiring Element is a relatively low-risk way – they’d get a working instrument without starting from scratch. It would echo QIAGEN’s earlier strategy (end-to-end NGS workflow for clinical use) but with a modern platform and without the IP overhang that GeneReader faced. This assumes Element is open to a sale and not already targeted by a bigger player like Thermo.

Pacific Biosciences – QIAGEN could take a different tack and acquire PacBio for its long-read capabilities. PacBio’s HiFi reads have value in clinical genetics (e.g. detecting structural variants, resolving complex regions that short reads miss). QIAGEN could package PacBio’s sequencers with its own sample prep and variant interpretation pipelines for applications like rare disease diagnostics. The complementarity is there (PacBio provides the data, QIAGEN provides the prep and analysis). However, PacBio’s focus historically has been research, and it might require significant effort to adapt it fully to high-throughput clinical testing. Moreover, PacBio’s price volatility and SoftBank’s involvement add complexity. Still, given PacBio’s low valuation now, QIAGEN could feasibly attempt a takeover (perhaps in partnership with a private equity backer). Verdict: Low-to-moderate probability. This would be a bold move for QIAGEN, transforming it into an instrument company overnight. It makes strategic sense if QIAGEN believes long-read sequencing will be a cornerstone of future diagnostics – they would gain a unique asset and not have to rely on Illumina/others. On the flip side, it’s a heavy lift for QIAGEN’s finances and organization, and they walked away from building a much simpler short-read system in 2019. Thus, while possible (especially if PacBio actively seeks a buyer), QIAGEN might be cautious here unless it feels compelled to secure a long-read platform before competitors do.

Oxford Nanopore – ONT’s rapid sequencing could synergize with QIAGEN’s strength in sample prep for infectious disease and human ID testing. For example, QIAGEN could combine its DNA extraction kits and QIAstat diagnostic assays with ONT’s MinION/PromethION for comprehensive analysis in outbreaks or for pharmacogenomics. However, ONT is a larger and arguably more complex target (with proprietary hardware, ASICs, and chemistry). It also already has partnerships (and its own commercial team). QIAGEN might find ONT a bit outside its core competency to operate. Verdict: Low probability. A partnership (QIAGEN providing prep kits to ONT users, which is already happening to some extent) is more likely than an outright acquisition in the near term.

Ultima Genomics – Ultima’s ultra-high-throughput model (flow-through sequencing) is geared towards population-scale genomics, which is not QIAGEN’s typical market (QIAGEN focuses more on targeted panels and medium throughput diagnostics). It’s unlikely QIAGEN would pursue Ultima, as Ultima’s value proposition (cheapest cost per genome) shines in large projects, not necessarily in the bread-and-butter clinical tests QIAGEN sells. Also, Ultima is still proving its technology, and QIAGEN tends to be risk-averse on unproven platforms.

QIAGEN Summary: QIAGEN’s strong clinical assay business gives it motive to integrate a sequencing platform, but its past experience counsels caution. We see a moderate chance that QIAGEN will acquire a smaller short-read platform like Element Biosciences to offer a one-stop NGS solution for clinical labs (reviving the GeneReader concept with better tech). This would align with QIAGEN’s strategy of enabling “sample to insight” workflows. An acquisition of a long-read player (PacBio or ONT) is less certain, but cannot be ruled out if QIAGEN decides that unique sequencing capabilities are critical to its future diagnostics portfolio – particularly given Illumina’s dominance and the need for differentiation. Overall, QIAGEN is likely a second-tier contender in the M&A race – they will move if the price and timing are right, but may also find partnerships (with Illumina, ONT, etc.) an easier route than large-scale acquisition.

Revvity (PerkinElmer)

Revvity Inc. – the new branding for PerkinElmer’s life-science and diagnostics business – is an interesting case. Revvity/PerkinElmer has deep roots in diagnostics (newborn screening, reproductive genetics, infectious disease testing) and in life-science tools (imaging, automation, reagents). They even operate a clinical genomics lab service (PerkinElmer Genomics) for genetic testing. Despite this, PerkinElmer historically did not develop an NGS instrument of its own; instead, it supplied sample prep chemistries and genomic testing kits. With the reorganization into Revvity, the company signaled a focus on “forces uniting human health” (multi-omics, diagnostics, etc.), which could imply interest in adding NGS to its arsenal.

Potential acquisition considerations for Revvity:

Mid-tier NGS platforms (Element or ONT) – Revvity could target an accessible, proven NGS platform to integrate with its diagnostic kits. For example, Element Biosciences might appeal here as well, for similar reasons it would to QIAGEN. Revvity could bundle Element’s sequencer with its chemistries for applications like inherited disease testing or oncology panels, areas where PerkinElmer/Revvity has content. The company has made acquisitions in the past in the low billions (e.g. Euroimmun for ~$1.3B in 2017, Oxford Immunotec for ~$591M in 2021), so a deal in the sub-$1B range is plausible. Verdict: Moderate possibility – if Element doesn’t get scooped by a larger player, Revvity might see it as a chance to obtain NGS tech and differentiate its offerings in prenatal or neonatal genomic screening (where NGS is becoming important). Revvity’s financial capacity is lower than Thermo or Danaher, so it will likely avoid a bidding war for any hot asset.

Specialized multi-omics tools – While 10x Genomics would be a transformational acquisition giving Revvity a big play in single-cell, it’s likely too large a bite (10x’s $1B+ size and high-profile nature means competition from bigger suitors). Revvity might instead look at smaller spatial omics companies or complementary tech that ties into NGS (for instance, companies in the long-read PCR or targeted sequencing space that bolster its diagnostic menu). None of the listed NGS-focused targets except perhaps Element clearly fit this “small tuck-in” profile.

PacBio or ONT – These seem less likely for Revvity. PacBio’s long-read platform could enhance Revvity’s clinical genomics lab (e.g. helping diagnose genetic disorders with structural variants), but integrating and supporting a global sequencer install base might be beyond Revvity’s current scope. ONT likewise would be a major undertaking, and ONT’s direct sales model and frequent updates might not mesh well with Revvity’s style. Unless Revvity aims to catapult itself into the big leagues of sequencing overnight (which would be a risky strategy), it will probably not pursue these larger targets.

Revvity Summary: Revvity’s strong foothold in clinical testing means it stands to benefit from NGS technology, but as an acquirer it will be selective. Of the major NGS players, Element Biosciences (or a similar small short-read company) stands out as a reasonable target that Revvity could integrate to complement its diagnostic kits. This would allow Revvity to offer end-to-end solutions, say, for newborn genomic screening or hereditary disease testing using NGS, leveraging its assay expertise with an owned instrument. We rate the likelihood of a Revvity NGS acquisition as moderate – not as assured as Thermo or Danaher, but definitely possible if the right opportunity (and price) presents. Revvity will also be influenced by what larger competitors do; if Thermo and others start consolidating NGS assets, Revvity may feel pressure to secure a platform to avoid being reliant on competitors for sequencing technology.

bioMérieux

bioMérieux is a French diagnostics powerhouse, specializing in clinical microbiology (e.g. blood culture, microbial identification, and the BioFire multiplex PCR system for infectious disease). bioMérieux has a clear focus on clinical assays, and NGS has begun to penetrate that domain (for example, hospital labs performing whole-genome sequencing of bacteria for outbreak tracking). Indeed, bioMérieux has already dabbled in NGS via partnerships – notably a co-development agreement with Illumina to create the EpiSeq™ service for hospital infection control, which combines Illumina’s MiSeq sequencer with bioMérieux’s pathogen database for epidemiological analysis. This indicates bioMérieux recognizes the value of NGS in its field.

The question is whether bioMérieux would acquire an NGS company outright. A few factors to consider:

bioMérieux’s strategic focus is providing turnkey diagnostic solutions to clinical labs. Any sequencing platform it offers would likely need to be bundled with easy workflows and specific diagnostic applications (much like how BioFire provides a complete sample-to-answer solution). Standalone sequencers meant for researchers are less of interest unless they can be adapted to clinical use.

Oxford Nanopore Technologies (ONT) – ONT’s technology could be a strong match for bioMérieux’s infectious disease franchise. ONT devices (MinION, GridION) are already used for rapid pathogen identification and genomics (e.g. real-time sequencing of hospital outbreaks, viral surveillance). ONT’s portability and speed align with the needs of clinical microbiology labs that require quick turnaround. bioMérieux could conceivably acquire ONT and develop dedicated clinical assays on its nanopore platform – for instance, rapid NGS-based tests for sepsis pathogens or drug-resistance genes, leveraging ONT’s ability to sequence directly from sample in a matter of hours. Additionally, ONT’s products are CE-marked and some have begun attaining regulatory approvals, smoothing the path for clinical adoption. Financially, ONT (market cap ~$1.3–1.5B) is within bioMérieux’s reach (bioMérieux SA’s market cap is around €12B). The Mérieux family, which controls the company, has historically made bold moves (like the $450M acquisition of BioFire in 2014). Verdict: Moderate probability. If bioMérieux wants to own an NGS platform, ONT is arguably the best fit given its focus on infectious disease use cases. However, politics could play a role – ONT is a UK-based “national champion” in genomics, so a foreign takeover might face scrutiny. Also, bioMérieux would need to ensure it can dedicate resources to support and evolve ONT’s technology post-acquisition, which is a significant commitment. It might be more likely to see a strategic alliance or minority investment first. But as Western companies consolidate, bioMérieux might act to secure ONT and keep it out of competitors’ hands, especially with Chinese firms out of contention.

Element Biosciences or other short-read platforms – bioMérieux could consider a benchtop short-read sequencer (like Element) to integrate into clinical lab workflows for applications like bacterial genome sequencing or oncology diagnostics (areas the company has some presence in). If, for example, bioMérieux wanted to offer a genomic profiling service for antibiotic resistance, it could bundle an Element sequencer with its sample prep and informatics. Still, this is a bit outside bioMérieux’s core, and Illumina’s platforms are already widespread in those labs. bioMérieux might prefer partnering with Illumina (as it has done) rather than owning the instrument manufacturing business.

PacBio – PacBio’s long-read tech could theoretically be useful for microbial genomics (giving complete closed genomes of pathogens) and for certain clinical genomics areas. But PacBio sequencers are higher-cost and slower, which doesn’t align well with routine clinical lab needs (where turnaround time and cost per test are critical). It’s unlikely bioMérieux would pursue PacBio, especially since PacBio is more research-oriented at present.

Singular Genomics – This company pivoted to spatial sequencing and has been acquired by a private investor, so it’s essentially off the table for now. In any case, its focus isn’t directly synergistic with bioMérieux’s main business.

bioMérieux Summary: With a strong clinical assay business in infectious disease, bioMérieux will look at NGS through the lens of clinical utility and integrated solutions. The most compelling scenario is bioMérieux acquiring Oxford Nanopore to build a rapid clinical sequencing platform for infection diagnostics. This would leverage both companies’ strengths – bioMérieux’s assay development and clinical market access, and ONT’s real-time sequencing – at a time when no Chinese competitor can intervene (MGI is hampered by patents/geopolitics, and Illumina is occupied with other issues). We rate this scenario as moderately likely. BioMérieux could also simply continue partnering with Illumina or ONT rather than acquiring; an acquisition would only happen if bioMérieux feels owning the tech gives a clear competitive edge (and if ONT’s price is attractive enough). In summary, while not as certain as Thermo or Danaher moves, bioMérieux is a potential surprise buyer of an NGS company, particularly one with strong infectious disease sequencing capabilities.

Bruker Corporation

Bruker is predominantly known for its advanced analytical instruments (mass spectrometers, NMR systems, imaging, etc.) and for its MALDI-TOF mass spec used in clinical microbiology (the MALDI Biotyper). Bruker has a foothold in the “omics” world through proteomics and metabolomics, but has so far not been a player in genomics. Would Bruker jump into NGS via M&A? A few points:

Bruker’s strategic direction has been to expand in high-end instrumentation and multi-omics. They have recently invested in areas like proteomics (e.g. acquiring PreOmics for sample prep) and spatial biology (e.g. a partnership with Canopy Biosciences). Genomics might be seen as a missing piece in a full multi-omics offering.

However, NGS instrument development and support are quite different from Bruker’s typical products. Bruker sells relatively low-volume, high-cost machines to specialized labs (and service contracts thereafter). NGS platforms, in contrast, can have larger install bases and require continuous chemistry and software updates. This might not align well with Bruker’s operating model.

If Bruker were to consider an acquisition, it might look at something that overlaps with its current markets. One possibility is Oxford Nanopore or another single-molecule sequencer, since Bruker could conceptually integrate nanopore sequencing with its single-molecule detection expertise (Bruker’s CEO has even alluded to single-molecule protein sequencing as an interest; nanopore DNA sequencing is tangentially related). But ONT is fairly large and not an obvious target for Bruker, and again, supporting a DNA sequencing platform might be a stretch.

Bruker might also consider smaller tech that complements its microbiology line. For instance, a company offering sequencing-based microbial strain typing or antibiotic resistance testing could fit. None of the listed major NGS players fits that niche exactly (though ONT could be used for it). Perhaps Bruker would be more inclined to partner (e.g. connecting their MALDI results with sequencing results in software) than to acquire a platform.

Financially, Bruker (market cap ~$10B) could manage a mid-size acquisition, but it tends to favor bolt-ons in its core areas rather than big transformative deals.

Bruker Summary: We view a major NGS acquisition by Bruker as least likely among the companies discussed. While Bruker certainly has the scientific know-how to appreciate cutting-edge sequencing technology, it has not signaled any intent to enter that market. Its resources are also smaller than Thermo’s or Danaher’s, so it would likely get outbid for attractive targets. If anything, Bruker might pursue partnerships to incorporate genomic data into its multi-omics pipelines. Unless Bruker identifies a very specific sequencing technology that complements its portfolio (and that others aren’t vying for), it probably will not make a big NGS M&A move in the next year or two.

Bio-Rad Laboratories

Bio-Rad straddles the research and clinical diagnostics spaces with a variety of products: gel electrophoresis, PCR (it co-developed the first qPCR), droplet digital PCR (ddPCR, through its RainDance acquisition), and clinical diagnostics reagents (like quality controls, blood typing, etc.). Notably, Bio-Rad was embroiled in a long patent war with 10x Genomics over microfluidic technology used for single-cell sequencing. That dispute was settled in 2021 with a global cross-license agreement, meaning Bio-Rad and 10x now have a truce and the freedom to use each other’s IP in certain areas. This development potentially opens the door for closer collaboration – or even a combination – between Bio-Rad and 10x.

Here’s how Bio-Rad might factor into NGS/Multi-omics M&A:

10x Genomics – As discussed, 10x is a prime target in the genomics tools arena. If Danaher (the odds-on favorite) were for some reason to hold off, Bio-Rad could be a contender to acquire 10x Genomics. Bio-Rad has a history in microfluidics (it acquired droplet tech companies and also a single-cell analysis company Celsee), and it indirectly owns a stake in 10x via its large shareholding in Sartorius AG, which in turn invested in 10x during its IPO. An acquisition would give Bio-Rad a dominant position in single-cell genomics, leveraging the very IP that was once disputed. The strategic fit: Bio-Rad’s expertise in precision microfluidics and PCR could complement 10x’s single-cell and spatial platforms, and Bio-Rad’s global distribution in research labs could help 10x reach more customers. Financially, Bio-Rad has a hidden war chest in its $11B stake in Sartorius – it could potentially monetize part of that to fund a purchase of 10x ($1–2B range currently). Culturally, 10x is a fast-moving Silicon Valley company, which might clash with Bio-Rad’s steadier approach, but with the patent peace in place, integration is at least legally feasible now. Verdict: Moderate probability. If Danaher forgoes 10x or faces antitrust hurdles (though none obvious, since Danaher isn’t in single-cell yet), Bio-Rad might step in. It would be a significant shift for Bio-Rad, turning it into a major genomics player overnight. This could be appealing as a growth avenue, given some of Bio-Rad’s traditional businesses are mature. Still, Bio-Rad is typically more conservative with M&A than Danaher/Thermo, so it’s not the top likelihood, but it’s one to watch.

NGS Platforms (Element, others) – Bio-Rad so far hasn’t shown interest in owning a sequencer. It focuses on genomics upstream (PCR, library prep) and downstream (data analysis software via subsidiaries), but not the actual sequencing step. That said, if Bio-Rad wanted to round out a complete genomics workflow, it could consider a small platform like Element. More intriguingly, Bio-Rad’s ddPCR is sometimes seen as complementary or a competitor to NGS for certain applications (liquid biopsy mutation detection, for example). Bio-Rad might prefer to double down on ddPCR rather than enter the crowded NGS instrument market. We haven’t seen strong signals of Bio-Rad courting any NGS manufacturer, so this remains speculative.

Multi-omics integration – Bio-Rad might also look at companies bridging genomics with proteomics or other omics. For example, 10x Genomics (again) has protein + gene expression kits (feature barcoding technology) – another reason 10x is a multifaceted catch. Other multi-omics startups (like those in spatial proteomics) could be on Bio-Rad’s radar, but those are outside our current scope.

Bio-Rad Summary: Bio-Rad’s large installed base in genomics labs and its droplet microfluidics know-how put it in a position to consider an acquisition like 10x Genomics, which would greatly enhance its multi-omics portfolio. We consider Bio-Rad a dark horse candidate: not the first name that comes up for NGS M&A, but one that could surprise the market by snapping up a key player like 10x if the fit and timing are right. The geopolitical climate (Chinese players sidelined) and the relative affordability of targets strengthen Bio-Rad’s hand. Outside of a 10x scenario, we don’t foresee Bio-Rad aggressively chasing other NGS companies in the immediate term. It is more likely to continue focusing on incremental innovations (like expanding its ddPCR applications) unless a truly strategic asset becomes available at a compelling price.