Oxford Nanopore FY23 Results

Oxford Nanopore FY23 Results

Look away now if you are here for the noise

Oxford Nanopore has presented FY23 Results, and here are my highlights.

The company sells Next-Generation Sequencing (NGS) Life Science and Research Technologies (LSRT) in the shape of instruments and reagents. The company benefited from the need for highly deployable viral surveillance and monitoring setups during the 2020-2022 COVID19 pandemic, but now it’s back to normal after the winding down of COVID19 operations globally.

The main highlight here is that 3/4 of the LSRT revenue is in reagents, which is one of the main selling points for ONT: our instruments are close to CAPEX zero, and thus can be made highly deployable. Hence the motto: “sequence anything, anywhere”.

The other highlight is that the company now has $600M in cash and have a $1.35B valuation (at £1.25 share price), which means they are at around $750M EV. But given that their revenue is 75% consumables, out of the $216.27M total, they are making $160M in consumables revenue, making their EV 4.68x to that consumables revenue.

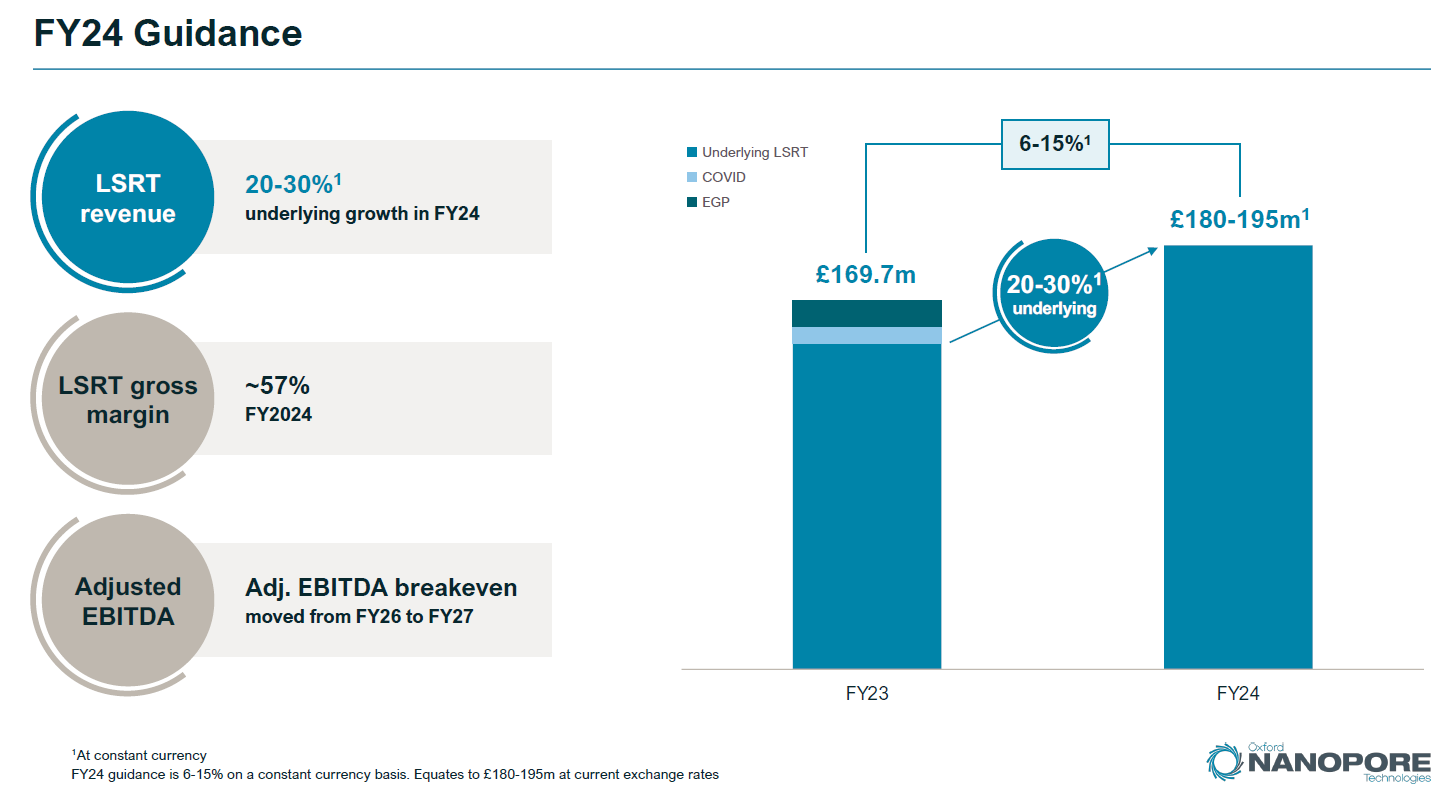

The all important guidance numbers are for a 20-30% growth in FY24, with a ~57% gross margin.

The company also aims at a 10-20% of LSRT revenue from clinical and applied industrial markets in 2026. I don’t think that’s too ambitious, as “applied markets” here could be something as simple as mRNA vaccine manufacturing QC.

Some more details on the finance, with the $600M cash figure.

Interesting numbers from the Americas: their revenue is smaller than EMEAI, which I believe remains an outlier in the world of NGS. I’ll discuss more around this in the ‘Strategic Positioning’ part of this post.